Top Plumbing Segments That Benefit Most from Plumbers’ Insurance

Every plumbing business faces risks—water damage from a failed fitting, a torch-related fire during a repipe, a client slip-and-fall, or a sewer backup that leads to bacterial or mold claims. Plumbers Insurance is the contractor‑tailored package that addresses these exposures. It’s typically anchored by general liability (GL) and rounded out with tools & equipment (inland marine), commercial auto, workers’ comp, and often contractors’ pollution liability (CPL) and professional liability/E&O. While not always mandated by law, proof of coverage is frequently required by clients, landlords, and many cities/counties before issuing licenses or permits.

Below are the types of plumbing work that benefit most—and the coverages that matter for each.

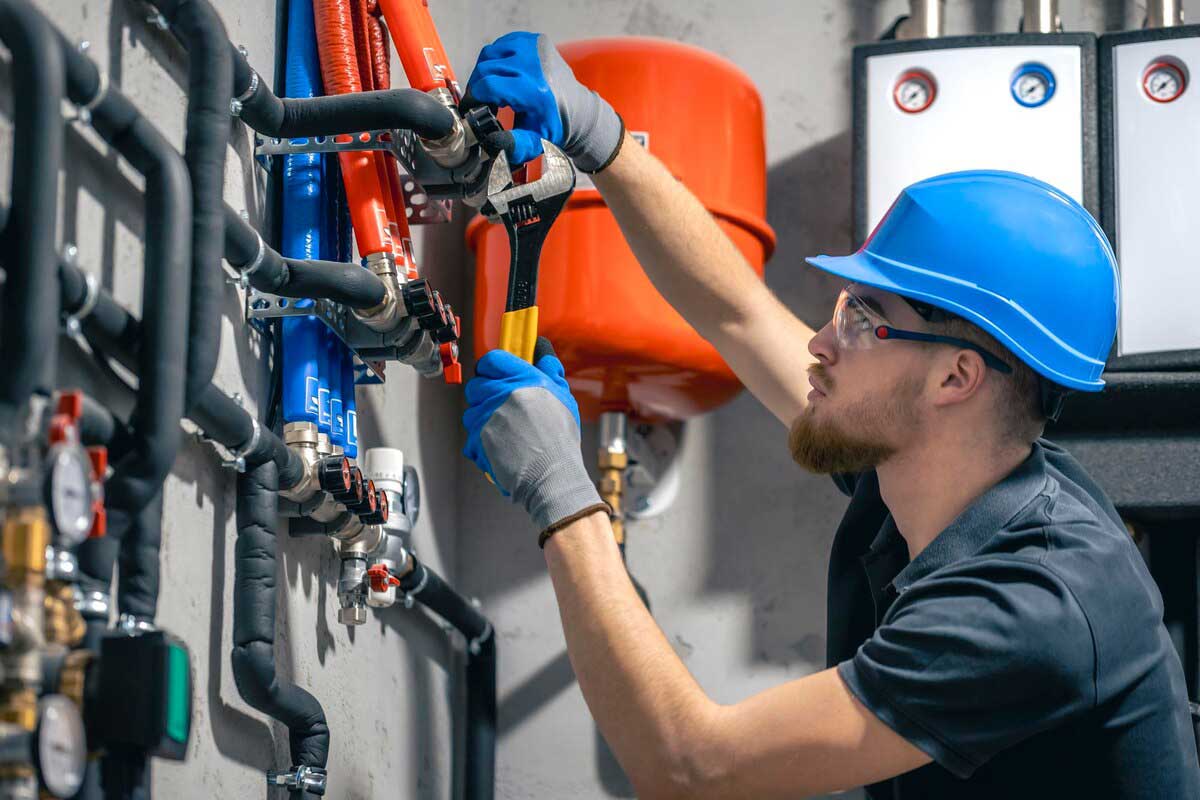

1) Residential Service & Repair

Why it matters: You’re in occupied homes where slip‑and‑falls, accidental water damage, and allegations of advertising injury can occur. Tools are mobile and prone to theft; vans are on the road daily.

Examples: A burst supply line floods a kitchen; a customer trips in your work area; a sewer auger damages the flooring.

Key coverage:

- GL for third‑party bodily injury, property damage, and personal/advertising injury (typically occurrence‑based).

- Tools & Equipment (Inland Marine) for press tools, sewer cameras, job‑box contents—on the truck, in transit, or at a jobsite.

- Commercial Auto for at‑fault accidents; GL does not cover auto.

2) Kitchen & Bath Remodels / Repipes

Why it matters: Hot work (soldering/brazing) and open systems increase fire and water‑damage risk inside finished structures.

Examples: A torch ignites surrounding material; a missed shutoff causes water damage during reconnection.

Key coverage:

- GL incl. products‑completed operations for damage arising after you leave the site.

- CPL for exclusions tied to mold/bacteria/sewage—not reliably covered by standard GL.

- Risk controls to cut premiums: formal Hot Work and Wet Work/pressure‑testing permit programs.

3) New Construction (Residential)

Why it matters: Most claims come from completed operations—leaks discovered after turnover. GCs/owners often require specific limits and Additional Insured endorsements before you can start.

Examples: A slow leak from an installed line can cause ceiling damage months later.

Key coverage:

- GL with completed‑ops and AI endorsements (e.g., CG 20 37 for completed operations).

- Municipal/agency requirements: Many jurisdictions require a COI to license/register contractors or pull permits.

4) Commercial & Multifamily / Hospitality Jobs

Why it matters: Larger properties mean bigger water‑damage losses and tighter contract insurance language (higher limits, primary & non‑contributory, waivers). Umbrella/excess may be requested.

Market context 2025: Overall rates have moderated, but casualty (liability) still trends up, and auto/umbrella remain challenging—driven in part by “nuclear verdicts.”

5) Drain Cleaning, Hydro‑Jetting & Trenchless Sewer

Why it matters: Exposure to sewage and bacteria, underground work, and potential pollution implications.

Key coverage:

- CPL for bacteria/mold/sewage events commonly excluded from GL.

- Tools & Equipment (Inland Marine) for jetters, cameras, and locators.

6) Gas Piping, Boilers, Water Heaters & Hydronics

Why it matters: Fire/explosion and scalding exposures; hot‑work needed in tight spaces.

Key coverage:

- GL for third‑party injury/property damage; implement Hot Work controls to reduce losses and satisfy underwriters.

- E&O if you design/spec systems (sizing, venting, layout) that clients rely on. (E&O is commonly claims‑made.)

7) Municipal, Healthcare & Industrial Projects

Why it matters: Contracts often mandate specific GL limits, AI status, waivers, and sometimes additional lines (e.g., pollution). Many cities require contractor registration with COI—some even request additional insured language.

Examples: City work orders, hospital retrofits, water district upgrades.

Key coverage: GL (with contract‑compliant endorsements), CPL where required, and Umbrella/Excess for higher limits.

Key Coverages, At A Glance

- General Liability (GL/CGL): third‑party bodily injury, property damage, personal & advertising injury; usually occurrence‑based. Note: GL excludes your faulty workmanship costs and most pollution claims.

- Products‑Completed Operations: core for plumbers—responds to BI/PD after your work is finished.

- Tools & Equipment (Inland Marine): mobile gear in trucks/jobbies; theft, accidental damage, vandalism.

- Commercial Auto: liability/physical damage for business vehicles; GL won’t cover auto accidents.

- Workers’ Compensation: required in most states when you have employees. (Licensing bodies and cities frequently verify WC and GL.)

- Contractors Pollution Liability (CPL): fills GL’s mold/bacteria/sewage gap.

- Professional Liability/E&O: for design/spec/advice errors—usually claims‑made.

Broader Trends & Market Context (2025)

- Rates are easing overall, but casualty is an exception. Global commercial rates fell ~4% in Q2‑2025 overall; casualty rates rose about 4% globally and about 9% in the US.

- US pricing remains elevated, but is softening: CIAB surveys indicate average quarterly increases of 4.2% in Q1 2025 and 3.7% in Q2 2025—the 31st consecutive quarter of increases.

- Commercial auto and umbrella remain firm, pressured by social inflation and nuclear verdicts; contractors draw heightened underwriting scrutiny (drivers, water‑damage controls, contract terms).

Frequently Asked Questions

Is Plumbers Insurance legally required?

There’s no single federal mandate for “plumbers insurance,” but many states/cities require GL and a COI to license/register contractors or pull permits. Workers’ comp is required in most states when you have employees. Always check your local rules.

How much GL coverage do plumbers typically carry?

A common baseline for small contractors is $1 million per occurrence / $2 million aggregate (often with higher limits on commercial jobs or through an umbrella policy).

What does Plumbers GL not cover?

It won’t cover auto accidents (that’s commercial auto), your own faulty work to redo/repair, most pollution events, or employee injuries (that’s workers’ comp).

Does it cover social media or advertising mistakes?

Yes—GL includes personal & advertising injury (e.g., slander/libel, copyright) subject to policy terms.

What does Tools & Equipment insurance add?

It protects movable tools (press tools, sewer cams, job‑box contents) against theft, vandalism, and accidental damage—coverage that fixed‑location property policies typically don’t provide.

Do plumbers need pollution coverage?

If you are exposed to sewage, mold/bacteria, or similar hazards (common in drain/sewer work, as well as water damage jobs), consider CPL because standard GL generally excludes these exposures.

What affects my premium the most?

Trade exposure (service vs. new construction), crew size/payroll, claims history, vehicles/drivers, state, and contract requirements. Typical GL snapshots for plumbers cost around $75–$115/month for smaller outfits (higher for larger crews/commercial work); bundle pricing can alter the total. Treat online averages as ballpark, not quotes.

Protect Your Plumbing Business the Smart Way

From residential service to heavy commercial, the right Plumbers Insurance mix—GL, tools & equipment, auto, workers’ comp, plus CPL/E&O where needed—keeps you compliant, contract‑ready, and resilient when the unexpected hits. Want tailored options and clear pricing?

Get a fast quote from Plumbers Insurance US and create a package that suits your jobs and budget.

General Liability Insurance US was created to solve a simple but frustrating problem: roofing business owners were spending hours trying to understand general liability insurance — comparing policies, deciphering jargon, and hoping they chose the right provider.